Welcome to this August 2021’s “CIO Office Monthly”, a new newsletter where Parkview’s CIO team offers their thoughts on global markets and provides their perspectives on what might be coming next.

In short:

- In the US and Europe, investors continue to “buy the dip”.

- China’s economic slowdown continues, and political interference is not helping.

- US treasury yields continue to fall, prompting a return to the status quo in equity markets.

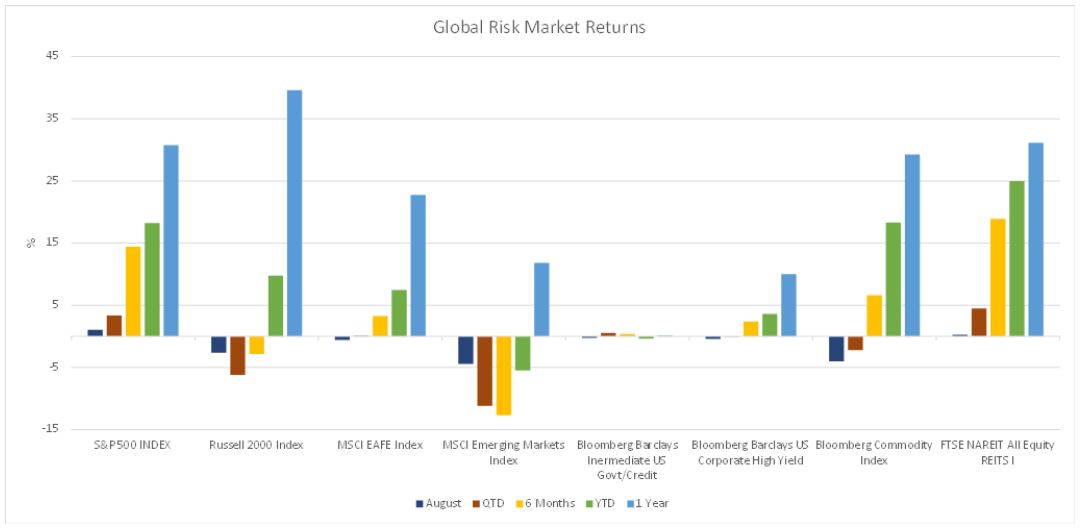

In the US, the spread of the Delta variant is extending the forecasted timeline for a return to normal. Globally, cases have been rising for 9 weeks in a row. Vaccination rates are slowing, but there is strong evidence that a combination of double vaccinations and community antibodies are slowing the spread – limiting harm this time around. The market is clearly pricing in lofty expectations for corporate earnings, given that we have now experienced a string of record earnings quarters. Not only is earnings growth off the charts, but we have seen a record proportion of companies in the US beating their consensus earnings expectations. US large cap stocks have continued to soldier on, with every bout of volatility in the index seemingly being chased by investors. But the overall trend the index masks some of the divergences between the underlying sectors and factors. More on this later.

Source: Bloomberg

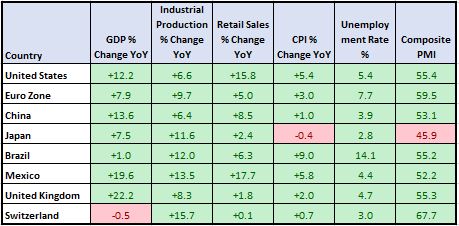

It has become quite clear that we have reached peak economic data in the US, Europe and China. We have entered a new period of more moderate data, as the initial economic recovery and year-on-year base effects are further behind us. Retail sales are slowing, as the US consumer shifts away from a goods economy back to a more conventional services based one. The pace of industrial production and durable goods new orders look to have slowed somewhat, after months of acceleration. Weaker responses in manufacturing purchasing manager surveys back this up. We have seen similar data from China, where the head start it had in the post-covid recovery now means that activity has been slowing for some time already. Interestingly, while Chinese PMIs are moderating alongside the U.S., PMIs are on the rise in Europe, indicating that the delayed recovery in the euro area could finally be gaining some momentum as lockdowns are finally falling away in the region.

As was largely expected, prices are higher. Consumer prices in the US for June and July increased 5.4% in both months, when compared to this time last year. This was driven by used car, housing food an energy prices. Even the core measure of the consumer price index, which strips out food and energy prices, was up 4.5% compared to last year. We expect much of this supply chain and pent-up demand driven inflation to be transitory, and are already seeing a sharp deceleration in some of the key drivers when compared to last month. However, we argue that structural factors point towards higher price levels over the long-term. A recent slow-down in existing home sales, driven potentially by elevated prices, could be forcing would-be buyers into the rental market. This could support a rebound in housing rental related prices. While this shouldn’t solely prevent a slowdown in headline CPI, it might serve to keep inflation readings more elevated than they would be otherwise. This will likely keep taper talk among hawkish Fed officials in the headlines.

Source: Bloomberg

US treasury yields have been falling sharply since April – casting doubt on the enthusiasm shown by equity investors. The bond market may be pricing in the decelerating economic activity highlighted above, or more nuanced dynamics such as the drawdown of the treasury general account. Instead of issuing as many new treasuries to fund new governmental spending, the US Treasury is currently drawing down its inflated general account at the Fed. This decrease in the supply of new Treasuries could be contributing to rising prices. Lower yields are helping longer duration equities in the tech and healthcare sectors – where earnings are expected further out in the future. This has led to a sector rotation back to the winners of the last 5 or so years, and away from cyclical, real economy companies that have outperformed during the covid recovery.