Während die Berichtssaison des ersten Quartals zu Ende geht, haben die Anleger einen gemischten Blick auf den Markt. Während das Wachstum des S&P 500 beim Gewinn pro Aktie (EPS) im Durchschnitt 25% betrug, wobei mehr als drei Viertel der Unternehmen die Analystenschätzungen übertrafen, stieg der Index seit Beginn der neuen Saison am 13. April nur um 50 Basispunkte.

Die Gründe für diese Inkohärenz sind vielfältig:

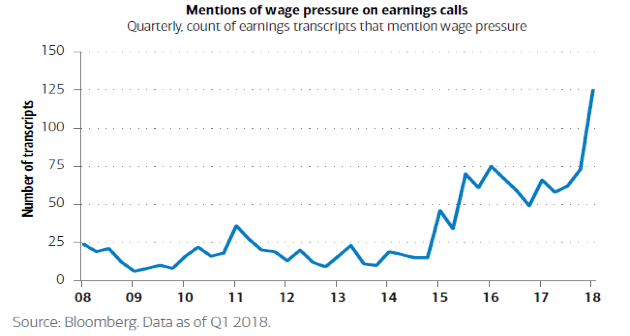

1. Der Arbeitsmarkt der Vereinigten Staaten befindet sich auf seinem niedrigsten Stand seit 17 Jahren, mit einer Arbeitslosenquote von 3,9%. Die amerikanischen Unternehmen kämpfen darum, Stellen zu besetzen; es wird geschätzt, dass es derzeit etwa 6 Millionen Stellenangebote gibt, von „Apfelpflückern bis zu Apple-Genies“. Obwohl das Lohnwachstum weiterhin langsam ist, scheint es eine wachsende Sorge zu sein, die in den kommenden Quartalen auf die Unternehmensmargen drücken könnte.

2. A low unemployment rate coupled with positive economic data and an inflation rate within target, all point to a continuity of the Fed’s hawkish stance. Higher rates increases downward pressure on equities as:

- Earnings yields became less attractive as investors substitute some of their equity exposure for cash

- It increases the borrowing costs and since many companies have accumulated cheap debt over the past few years, refinancing will become more expensive and would eat into company margins

- Part of the equity upside we’ve witnessed over the past couple of years has been fuelled by share buy-backs. Higher rates will limit the ability for companies to borrow cheaply to buy their own shares

3. Tax cuts introduced in December 2017 by the Trump administration helped push earnings this past quarter. In other words, part of the stellar results can be attributed to an artificial boost and not only to strong sales and company fundamentals. Tax cuts are less likely to contribute as much in the next quarter, as this event is now priced-in

4. Tax cuts and other reform change, like the easing of the Dodd-Frank bill, had already been priced-in. „Buy the rumour and sell the news“ seems to have limited the upside of the S&P 500 during the first quarter’s earnings season

5. Almost 30% of the S&P 500 revenue comes from abroad and a stronger USD may put downward pressure on future earnings. The USD is likely to remain strong as:

- The difference in monetary policy between the Fed and its Japanese and European peers means that the USD is a more attractive currency to hold

- On a Purchase Power Parity basis, the USD appears cheap and should continue to strengthen

- The US has always had a trade deficit which pushes the currency down and last month’s figure was the widest in 10 years. However, March reading shows that it has significantly narrowed and this may have added some strength to the USD

What this earnings season tells us is that fundamentals remain strong but it isn’t enough to satisfy investors. Geopolitical tensions, the prospect of a trade war and the flattening of the yield curve all point to an increase in uncertainty and weaker growth prospects. For the equity markets, this blurs the prospects of next quarter’s earnings.

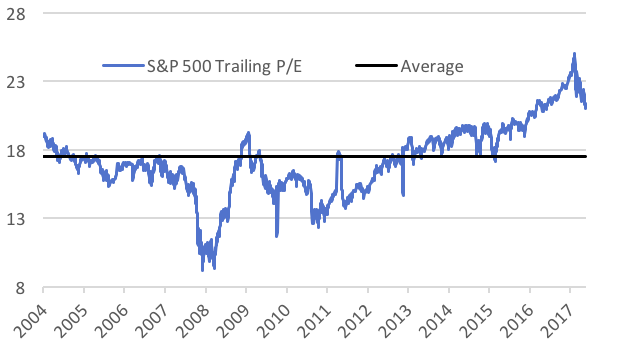

Auf der positiven Seite wurden die US-Bewertungen attraktiver. Die hohen Renditen zusammen mit stabilen Preisen bedeuten, dass das KGV auf nachhaltigere Niveaus zurückgekehrt ist, obwohl es immer noch über dem langfristigen Durchschnitt liegt. Unsere Untergewichtung in US-Aktien ermöglichte es uns, unser Engagement zu einem Zeitpunkt zu reduzieren, als Aktien teuer waren, und gibt uns Zeit, einen Wiedereinstieg zu planen. Allerdings bremsen derzeit externe Widrigkeiten die positive Wirkung der soliden Wirtschaftsdaten, und wir sehen kurzfristig ein begrenztes Aufwärtspotenzial, da die Bewertungen etwas substanziell bleiben. Daher halten wir aufgrund des Dargelegten unsere Strategie unverändert bei.