À mesure que la saison des résultats du premier trimestre touche à sa fin, les investisseurs se sont retrouvés avec une vision mitigée du marché. Alors que la croissance du S&P 500 en bénéfice par action (BPA) était de 25% en moyenne, avec plus de trois quarts des entreprises dépassant les estimations des analystes, l’indice n’a augmenté que de 50 points de base depuis le début de la nouvelle saison le 13 avril.

Les raisons de cette incohérence sont multiples :

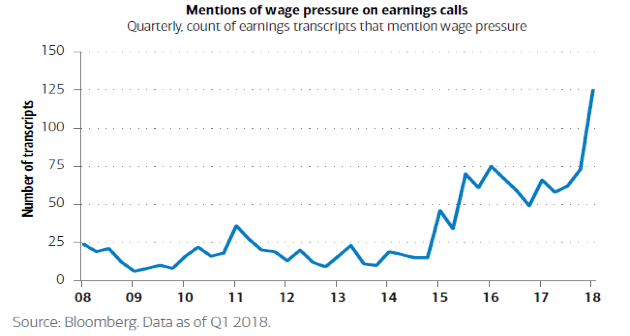

1. Le marché du travail des États-Unis est à son point le plus bas en 17 ans, avec un taux de chômage de 3,9%. Les entreprises américaines luttent pour pourvoir des postes ; on estime qu’il y a actuellement près de 6 millions d’offres d’emploi, des « cueilleurs de pommes aux génies d’Apple ». Bien que la croissance des salaires reste lente, elle semble être une préoccupation croissante qui pourrait peser sur les marges des entreprises dans les prochains trimestres.

2. A low unemployment rate coupled with positive economic data and an inflation rate within target, all point to a continuity of the Fed’s hawkish stance. Higher rates increases downward pressure on equities as:

- Earnings yields became less attractive as investors substitute some of their equity exposure for cash

- It increases the borrowing costs and since many companies have accumulated cheap debt over the past few years, refinancing will become more expensive and would eat into company margins

- Part of the equity upside we’ve witnessed over the past couple of years has been fuelled by share buy-backs. Higher rates will limit the ability for companies to borrow cheaply to buy their own shares

3. Tax cuts introduced in December 2017 by the Trump administration helped push earnings this past quarter. In other words, part of the stellar results can be attributed to an artificial boost and not only to strong sales and company fundamentals. Tax cuts are less likely to contribute as much in the next quarter, as this event is now priced-in

4. Tax cuts and other reform change, like the easing of the Dodd-Frank bill, had already been priced-in. « Buy the rumour and sell the news » seems to have limited the upside of the S&P 500 during the first quarter’s earnings season

5. Almost 30% of the S&P 500 revenue comes from abroad and a stronger USD may put downward pressure on future earnings. The USD is likely to remain strong as:

- The difference in monetary policy between the Fed and its Japanese and European peers means that the USD is a more attractive currency to hold

- On a Purchase Power Parity basis, the USD appears cheap and should continue to strengthen

- The US has always had a trade deficit which pushes the currency down and last month’s figure was the widest in 10 years. However, March reading shows that it has significantly narrowed and this may have added some strength to the USD

What this earnings season tells us is that fundamentals remain strong but it isn’t enough to satisfy investors. Geopolitical tensions, the prospect of a trade war and the flattening of the yield curve all point to an increase in uncertainty and weaker growth prospects. For the equity markets, this blurs the prospects of next quarter’s earnings.

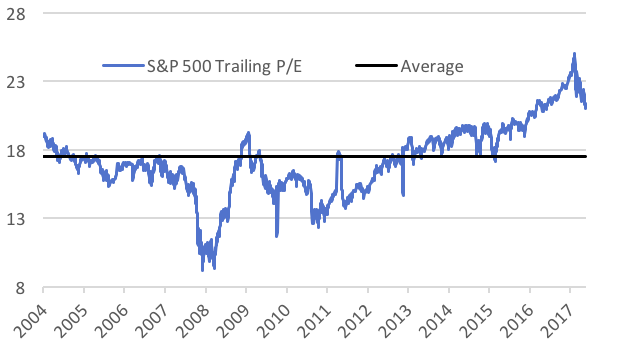

Du côté positif, les valorisations américaines sont devenues plus attractives. Les rendements élevés associés à des prix stables signifient que le PER est revenu à des niveaux plus soutenables, bien qu’encore au-dessus de la moyenne à long terme. Notre sous-pondération en actions américaines nous a permis de réduire notre exposition à un moment où les actions étaient chères et nous donne le temps de planifier un retour. Cependant, en ce moment, des adversités externes freinent l’impact positif des données économiques solides et nous voyons une hausse limitée à court terme avec des valorisations qui restent quelque peu substantielles. Par conséquent, compte tenu de ce qui précède, nous maintenons notre stratégie sans changements.